Watch this webinar on-demand now! Click here

Executive Summary

This webinar, co-hosted by the Green Economy Hub (VUCA Group) and Convergence Blended Finance, brought together leaders from the Green Climate Fund (GCF), Development Bank of Southern Africa (DBSA), InfraCredit Nigeria, and Climate Fund Managers (CFM) to unpack the current landscape of blended finance in Africa and highlight solutions that accelerate green and bankable project development.

Speakers emphasized that blended finance is a strategic, transitional tool designed to correct market failures, crowd in commercial capital, and build sustainable markets rather than replace private investment. Africa continues to represent half of global blended finance transactions, with strong activity across agriculture, financial services, energy, and increasingly climate-related infrastructure.

“Blended finance is transitionary in nature. It is meant to catalyse markets—not replace commercial capital.”

— Rajeev Mahajan, Green Climate Fund

Key Takeaways

1. Blended Finance Must Be Purpose-Built to Solve Specific Risks

Experts reinforced that concessionality should never be generic. Instruments—grants, guarantees, subordinated debt, TA, or viability gap funding—must be matched precisely to the underlying barrier, whether construction risk, creditworthiness of offtakers, project preparation gaps, or currency volatility.

2. Early-Stage Concessional Capital Is the Most Critical Missing Ingredient

Across all institutions, the biggest bottleneck remains the insufficient supply of early-stage, risk-tolerant capital required to turn concepts into bankable projects. CFM and DBSA highlighted how their project preparation and subordinated funding models address this structural gap.

3. Domestic Capital Mobilisation Is the Next Frontier

Nigeria’s InfraCredit demonstrated the power of guarantees to unlock pension and insurance capital for new asset classes such as distributed renewable energy. GCF stressed that local pension funds represent one of Africa’s strongest untapped pools of climate finance, especially because they operate in local currency.

4. Adaptation Finance Remains Hard — But Innovation Is Emerging

Projects in water, resilience infrastructure and agriculture still struggle due to unclear revenue models and public-sector complexities. CFM and GCF illustrated how demonstration projects, diversified portfolios, and tailored risk-sharing are starting to break through these barriers.

5. Market Creation Requires Partnership, Patience and Pipeline

Whether through DBSA’s Climate Finance Facility, CFM’s whole-life-cycle fund model, or GCF’s flexible, co-creation approach, panelists reinforced that the future lies in building replicable transaction structures that can scale across the continent.

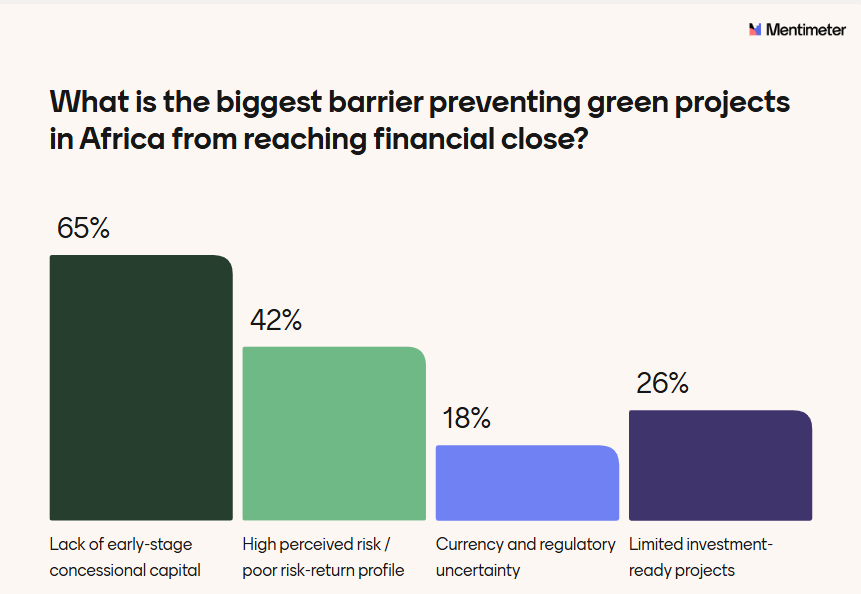

Insights From the Live Poll

Question: What is the biggest barrier preventing green projects in Africa from reaching financial close?

Top Answer: Lack of early-stage concessional capital (most votes)

This reinforces the consensus that project preparation, first-loss capital, and early-stage equity remain the most urgent gaps. It also validates why donors, DFIs and blended finance facilities should direct future resources toward pipeline development, feasibility studies, and catalytic first-loss structures.

Steps Moving Forward

1. Expand Project Preparation and Development Facilities

Scaling prep facilities—similar to CFM’s model—will accelerate the number of investment-ready projects on the continent.

2. Design More De-Risking Instruments for Local Investors

Guarantees, subordinated tranches, and credit-enhancement vehicles are essential to mobilise African pension funds and insurers.

3. Build Adaptation Business Models Through Demonstration Deals

High-quality early adaptation projects can prove viability and attract replication capital.

4. Improve Market Confidence Through Data, Reporting and Track Record

InfraCredit emphasised that consistent monitoring and transparency help domestic investors understand new asset classes and ultimately take more risk over time.

5. Strengthen Public–Private Collaboration on Policy and Tariff Reform

Developers cannot shoulder the risk alone; regulatory enablement is essential for scaling both mitigation and adaptation pipelines.

“If we can prove to pension fund managers that this asset class is de-risked, that money will flow—and it’s exactly the kind of long-term local currency capital we need.”

— Rajeev Mahajan, Green Climate Fund